The loss of a loved one is difficult enough without the added stress of navigating complex financial matters. For many, the question of an inheritance tax in Australia looms large, creating anxiety about unexpected bills and confusing obligations during an already challenging time. If you’re feeling overwhelmed by what you need to do or worried about making a mistake with the ATO, you are not alone, and we are here to provide clear, practical guidance.

Let us put your mind at ease. In this guide, we will give you the simple, direct answer you’re looking for regarding inheritance taxes in 2026. More importantly, we will walk you through the simple truth about the taxes that do apply when you inherit assets, such as Capital Gains Tax (CGT). Our goal is to demystify the process, replacing jargon and uncertainty with the confidence you need to manage your inheritance correctly and move forward with peace of mind.

The Short Answer: Does Australia Have an Inheritance Tax?

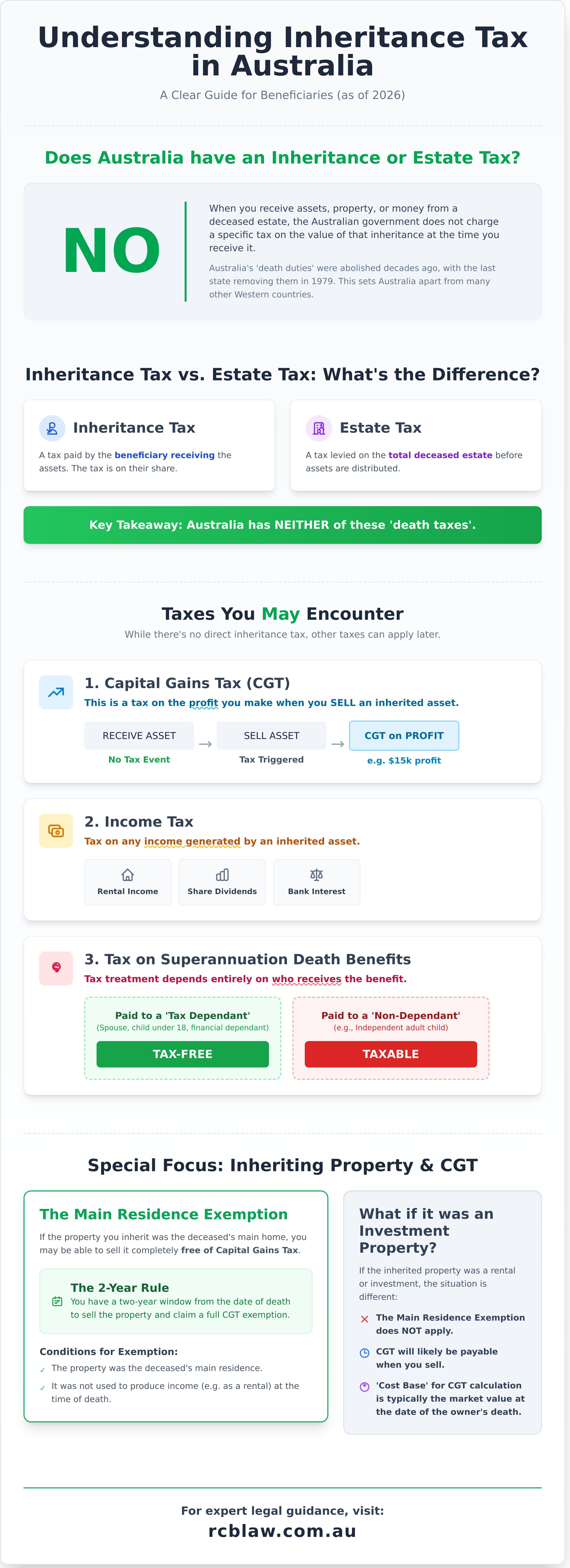

We understand that navigating the complexities of estate law can be stressful. So, let’s start with the most reassuring and straightforward answer: No, there is no inheritance tax australia.

This means that when you receive assets, property, or money from a deceased estate, the Australian government does not charge you a specific tax on the value of that inheritance at the time you receive it. You can inherit a A$1 million property or A$100,000 in cash, and you will not have a tax bill deducted directly from that amount.

Historically, Australia did have ‘death duties’ at both the federal and state levels. However, these were progressively abolished, with Queensland being the final state to remove them in 1979. For decades, the system of Taxation in Australia has operated without these levies, providing significant relief to beneficiaries. The complete absence of an inheritance tax australia sets the nation apart from many other Western countries.

Why is there so much confusion?

The confusion surrounding the topic of inheritance tax australia is common, and it often stems from a few key areas. Firstly, many of us are exposed to media and stories from countries like the United Kingdom and the United States, where inheritance or estate taxes are a significant part of estate planning. Secondly, the term is often used incorrectly in general conversation. Finally, the fact that other taxes, such as Capital Gains Tax (CGT), can apply later on when you sell an inherited asset often leads people to believe a direct inheritance tax exists.

Inheritance Tax vs. Estate Tax: Is there a difference?

While the terms are often used interchangeably, there is a technical difference. Understanding it can help provide further clarity:

- Inheritance Tax: This is a tax paid by the person or beneficiary receiving the inheritance. The rate can sometimes vary depending on the relationship to the deceased.

- Estate Tax: This is a tax levied directly on the deceased person’s total estate before the assets are distributed to the beneficiaries.

It’s a subtle but important distinction. However, the key takeaway remains the same: reassuringly, when it comes to a direct inheritance tax australia, neither of these “death taxes” currently exists.

The ‘Hidden’ Taxes: What You Actually Need to Know

While it’s a relief to know that a direct inheritance tax in Australia was abolished decades ago, this doesn’t mean that receiving an inheritance is always free from tax obligations. Understanding these potential taxes is not about causing alarm; it’s about empowering you with clear, practical knowledge. We understand this can be a complex area, and our goal is to provide the guidance you need to navigate the financial aspects of an inheritance with confidence.

Instead of a single inheritance tax, you may encounter taxes in three main areas.

Capital Gains Tax (CGT) on Inherited Assets

This is the most common tax beneficiaries face. Capital Gains Tax (CGT) is a tax on the profit you make when you sell an asset, not on the act of inheriting it. For example, if you inherit a portfolio of shares valued at A$50,000 and sell them a few years later for A$65,000, you may be liable for CGT on the A$15,000 capital gain. The key principle is that tax is only triggered by the disposal of the asset, not its receipt.

Income Tax on Earnings from Inherited Assets

If an asset you inherit generates its own income, that money becomes part of your assessable income for the year. As the Australian Taxation Office (ATO) clarifies, you must declare any income earned from the assets of a deceased estate. This income is then taxed at your personal marginal tax rate. Common examples include:

- Rental income from an inherited investment property.

- Dividends paid from inherited shares.

- Interest earned on funds held in an inherited bank account.

Tax on Superannuation Death Benefits

Superannuation follows its own set of rules and does not automatically form part of the deceased’s estate. The tax treatment depends entirely on who receives the benefit. If the super is paid to a ‘tax dependant’ (such as a spouse, a child under 18, or a financial dependant), the payment is generally tax-free. However, if the benefit is paid to a ‘non-dependant’, like an independent adult child, the taxable component of the superannuation payout may be subject to tax.

Inheriting Property: A Practical Guide to Capital Gains Tax

For many Australians, inheriting a property is the most significant part of a deceased estate. We understand this can be an emotional and complex time, and navigating the tax implications adds another layer of stress. While the good news is that there is no direct inheritance tax australia imposes, Capital Gains Tax (CGT) can apply when you eventually sell the asset. The key to managing this is understanding the main residence exemption.

The Main Residence Exemption: Your Key to a Tax-Free Inheritance

The most crucial rule to understand is the ‘main residence exemption’. In simple terms, if the property you inherit was the deceased’s primary home, you may be able to sell it without paying any CGT. The Australian Taxation Office provides detailed guidance, but the exemption generally applies if you sell the property within two years of the person’s death, provided it wasn’t used to generate income during that period.

- The Two-Year Rule: You have a two-year window from the date of death to sell the property and claim a full CGT exemption.

- Conditions: The home must have been the deceased’s main residence and not used to produce income (like a rental) at the time of their death.

What if the property was an investment?

If the inherited property was a rental or investment, the situation changes. The main residence exemption does not apply, and CGT will likely be payable when you sell. To calculate the tax, you’ll need to know its ‘cost base’. For an inherited asset, the cost base is typically the market value of the property at the date of the original owner’s death. This value becomes your starting point for calculating any capital gain or loss.

Partial Exemptions and Other Scenarios

Property inheritance isn’t always straightforward. If you decide to move into the inherited home and make it your main residence, you can claim the exemption for the period you live there. However, CGT may still apply to the period before you moved in. Similarly, if the property was used for both private and income-producing purposes (e.g., a home office or a granny flat was rented out), a partial CGT exemption may be available. These calculations can be intricate, highlighting why professional guidance is so valuable.

Navigating property law can be complex. Get expert advice from our conveyancing team.

How Proactive Estate Planning Can Protect Your Loved Ones

Understanding how your beneficiaries will be affected by your estate is only half the picture. The most significant step you can take is to plan your own affairs proactively. While the absence of a formal inheritance tax in Australia is a relief for many, it places even greater importance on meticulous estate planning. Without clear legal structures in place, your loved ones can face unintended tax consequences, confusion, and distressing family disputes.

A well-considered estate plan is not just about distributing assets; it’s about providing your family with security and peace of mind during a difficult time. It ensures your legacy is protected and passed on as you intended.

The Role of a Well-Drafted Will

A legally sound, professionally drafted will is the cornerstone of any effective estate plan. It provides absolute clarity on your wishes, significantly reducing the risk of conflict among beneficiaries. More than just a document, a will is a powerful tool that allows you to:

- Ensure assets are distributed correctly: Clearly outline who receives what, preventing ambiguity and potential legal challenges.

- Appoint a capable executor: Choose a trusted person or professional to manage your estate efficiently and compassionately.

- Help manage tax liabilities: Provide beneficiaries with the clarity needed to make timely decisions about assets, which can help in managing potential Capital Gains Tax (CGT) obligations.

Advanced Strategies: Testamentary Trusts

For those seeking greater control and protection for their beneficiaries, a testamentary trust can be a highly effective strategy. Established through your will, this type of trust comes into effect after you pass away. It offers significant advantages, such as protecting a beneficiary’s inheritance from creditors or relationship breakdowns and providing a tax-effective way to distribute income to younger family members, like grandchildren, for expenses such as education.

Why Professional Legal Advice is Crucial

While DIY will kits may seem like a simple, cost-effective option, they often create more problems than they solve. Vague wording, improper signing, or a failure to account for complex assets can lead to the will being contested or declared invalid. The resulting legal fees and family stress can far outweigh the initial savings.

Engaging an experienced lawyer ensures your will is not only legally valid but also strategically structured to reflect your true intentions. We understand that these matters are deeply personal and can be stressful. Our goal is to provide clear, concise support, helping you navigate the process to create a robust plan that safeguards your family’s future. To ensure your loved ones are protected, contact the experienced team at RCB Law for practical guidance.

Securing Your Legacy: Your Next Steps in Estate Planning

While the absence of a formal inheritance tax in Australia is welcome news, it doesn’t mean your estate is completely free from tax obligations. The key takeaways are clear: assets like property can still trigger Capital Gains Tax for your beneficiaries, and superannuation death benefits may also be taxed. The most powerful tool you have to navigate these rules is proactive, strategic estate planning, which ensures your wishes are honoured and your loved ones are protected from unnecessary financial stress.

Navigating this landscape can feel complex, but you don’t have to do it alone. With over 30 years of experience serving Queensland, the team at RCB Law provides specialist advice in Wills and Estates. We are dedicated to offering clear, stress-free legal guidance tailored to your unique circumstances. Ensure your assets are protected for the next generation. Contact RCB Law for expert will and estate planning advice. Taking proactive steps today provides peace of mind for tomorrow, ensuring your legacy is passed on exactly as you intended.

Frequently Asked Questions About Inheritance Tax

Do I have to pay tax on money I inherit from overseas in Australia?

While Australia does not have a direct inheritance tax, any income you earn from an inherited overseas asset is taxable here. For example, if you inherit a sum of money and place it in an Australian bank account, the interest earned is considered taxable income. Similarly, rental income from an inherited overseas property must be declared. You should also be aware that the country of origin may have its own estate or death duties that apply before the asset is transferred to you.

What is the ‘cost base’ of an inherited asset for CGT purposes?

The ‘cost base’ for an inherited asset is generally its market value on the date the person passed away. This value is crucial because it’s the figure you use to calculate Capital Gains Tax (CGT) if you later sell the asset. For instance, if you inherit a property valued at A$700,000 on the date of death and sell it years later for A$850,000, your capital gain would be calculated based on the A$150,000 difference, not the original purchase price.

Do I need to get a formal valuation of assets when someone passes away?

Yes, obtaining a formal valuation from a qualified professional is a critical step, especially for assets like real estate, shares, or valuable artworks. This valuation officially establishes the asset’s ‘cost base’ at the date of death. Having this formal documentation is essential for accurate Capital Gains Tax (CGT) calculations in the future and can prevent potential disputes with the Australian Taxation Office (ATO). It provides clear, defensible evidence of the asset’s worth at that specific time.

What is the difference between an executor of a will and a beneficiary?

An executor is the person or entity appointed in a will to administer the deceased’s estate. Their legal duty is to manage the process, which includes gathering assets, paying any debts, and distributing the remaining estate according to the will’s instructions. A beneficiary, on the other hand, is a person or entity who is set to receive assets or a benefit from the estate. It is common for a person, such as a spouse or child, to be appointed as both an executor and a beneficiary.

How long does it typically take to receive an inheritance after someone dies in Queensland?

The timeframe for receiving an inheritance can vary significantly, but in Queensland, it typically takes between 6 to 12 months. The process can be quicker for very simple estates with few assets. However, it may take longer if the estate is complex, requires a Grant of Probate, involves the sale of property, or if the will is challenged by a potential claimant. The executor must first settle all estate debts and tax obligations before any distribution to beneficiaries can occur.

Are gifts received before someone dies subject to any tax?

For the recipient, gifts are generally not subject to any tax. Australia does not have a “gift tax,” and this is consistent with the lack of a direct inheritance tax in Australia. However, there can be tax implications for the person giving the gift. If they gift an asset like property or shares, it may trigger a Capital Gains Tax (CGT) event for them. Furthermore, gifting can affect the giver’s Centrelink entitlements due to specific deprivation rules.